Berkeley Lab study investigates how plentiful electricity turns wholesale prices negative in the US

The year 2020 upended routines in nearly all aspects of our lives. In the realm of energy economics, we saw prices turn negative for U.S. crude oil, natural gas, and wholesale electricity. While negative prices were unprecedented for oil, similar conditions existed for natural gas in 2019, when pipeline capacity could not accommodate the rapid expansion of associated gas production in the Permian Basin. For electricity, which in comparison to oil and gas has negligible storage capacity, negative prices have been much more common and growing. Negative prices are interesting (and atypical for most commodities) because producers should theoretically cease production whenever sales prices fall below marginal production costs—let alone if negative prices require them to effectively pay (rather than be paid) to continue producing.

Berkeley Lab has published a short article in Advances in Applied Energy that examines the prevalence of negative prices in the United States in 2020, their genesis, and the implications for the broader electricity system.

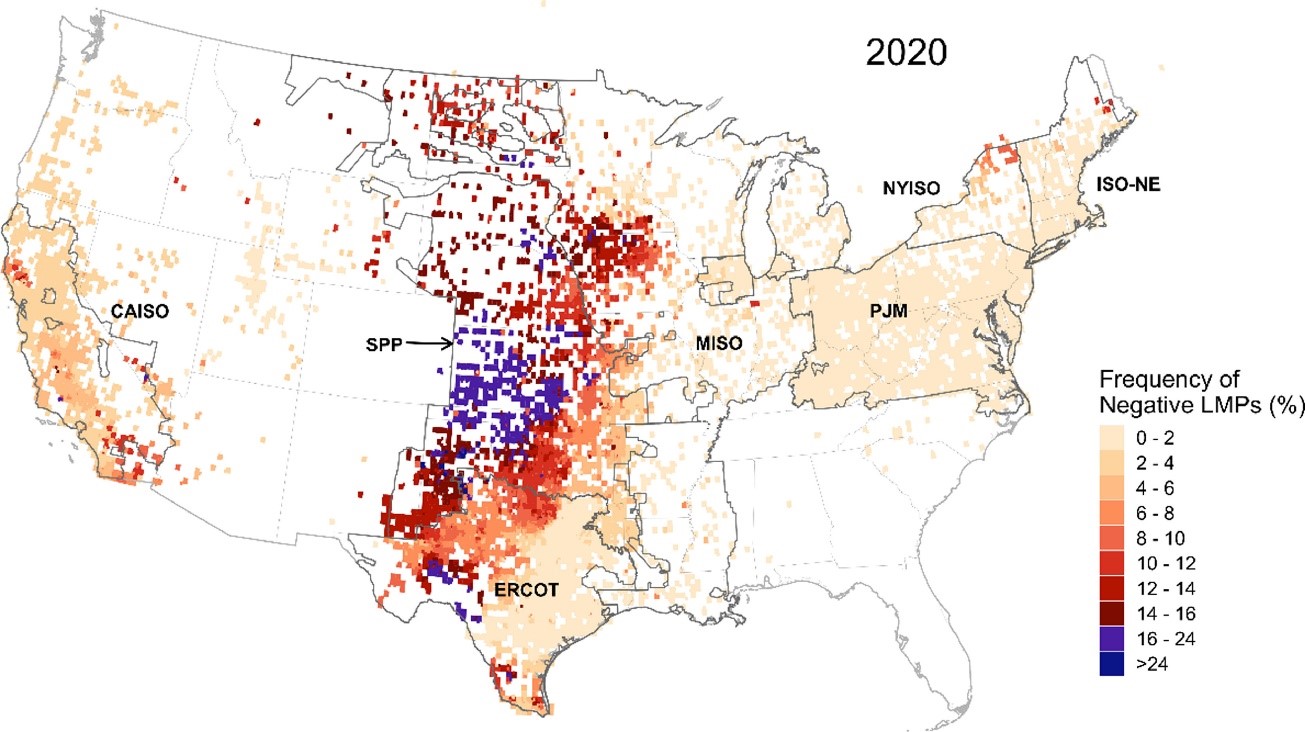

In 2020, average wholesale electricity prices in the United States fell to $21/MWh, their lowest level since the beginning of the 21st century. Low natural gas prices and the proliferation of low marginal cost resources like wind and solar had already established a trend toward lower wholesale prices, and this trend was augmented by declining electricity demand due to the Covid-19 pandemic in 2020. Negative real-time hourly wholesale prices occurred in about 4% of all hours and wholesale market nodes across the United States, but these were not distributed evenly. Regional clusters emerged, for example, in the Permian Basin in western Texas, and in Kansas and western Oklahoma in the Southwest Power Pool (SPP), negative prices accounted for more than 25% of all hours. In 2021, average wholesale energy prices have rebounded again in all ISOs by $10-$25/MWh, or even $70/MWh in ERCOT. But negative energy prices have either continued to grow modestly both in frequency and absolute magnitude (NYISO, ERCOT, and ISO-NE) or remained near 2020 levels (other ISOs). A caveat to this initial evaluation of 2021 trends is that the cited numbers only examine system-wide values at representative trading hubs, which do not reflect congestion costs at individual nodes.

Frequency of negative locational marginal prices at nodes in the seven organized wholesale markets in the United States in 2020.

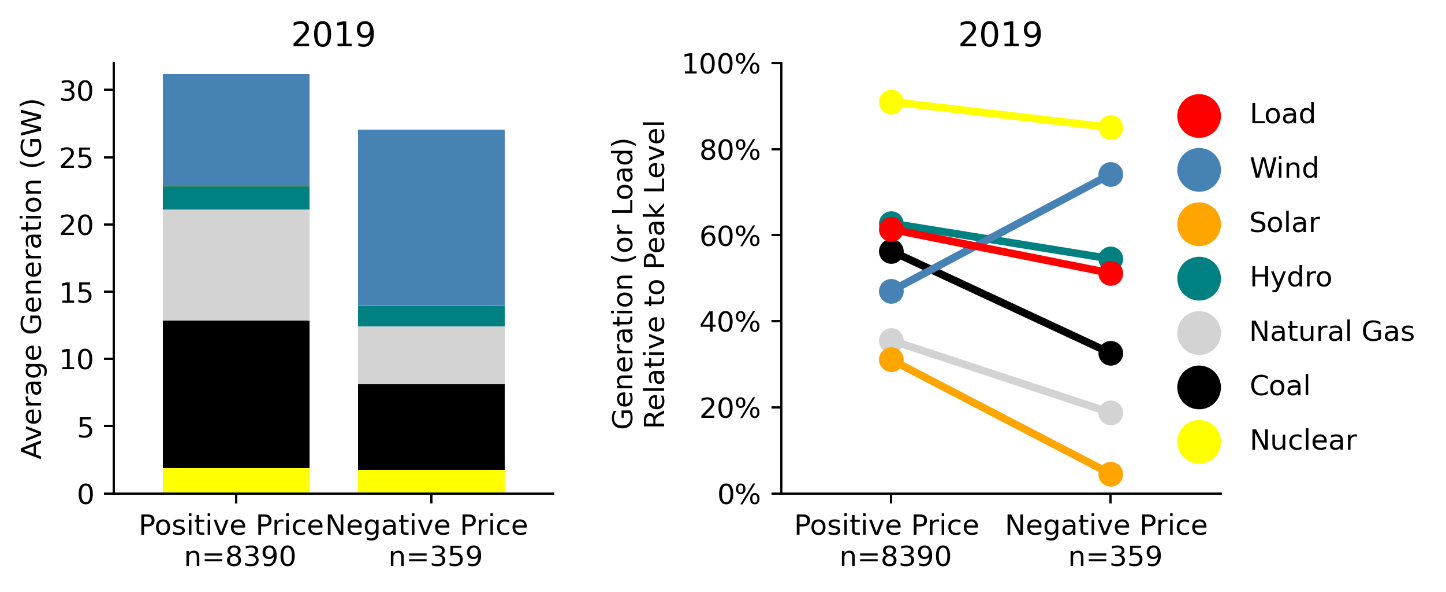

Negative electricity prices result either from local congestion of the transmission system leading supply to exceed demand locally or due to system-wide oversupply. Looking at the latter condition at SPP’s southern trading hub, we find that all major generator types contribute to this excess supply, because of limited ramping flexibility or self-scheduled out-of-market unit commitments. However, most generator types operate at lower production levels (or capacity factors) when prices turn negative. There are two notable exceptions: during negative price hours, nuclear projects continue to generate power at near-peak capacity levels and wind turbines generate at higher-than-average production levels—near 75% of their rated capacity. Monetary production incentives such as renewable energy credits or tax credits may facilitate negative bids of wind projects.

Average generation levels by fuel type in absolute (left) and relative (right) terms during positive and negative price hours at the southern trading hub in SPP in 2019 and 2020

We can highlight the shifting economic signals that negative electricity prices provide. For example, negative prices have implications for wind (and solar) deployment as they identify potential locations where the economic value of additional generation resources may have declined. They illustrate the possible need for, and value of, added transmission that allows excess electricity in one region with negative prices to reach distant demand centers in another region where electricity prices are positive. They suggest value in extracting more flexibility out of the conventional thermal fleet, especially from those generators that are not closely following economic signals. Related, storage in its various forms can add value by moderating temporal supply and demand imbalances. Finally, with different retail rate designs, more-impactful economic signals to end-use customers could alert them to the availability of low-priced electricity, allowing them to shift demand in time or between locations. Large flexible energy consumers may have the opportunity to reduce their operational costs by availing themselves of plentiful and cheap energy.

If you want to dive deeper, you can freely access our short article in Advances in Applied. You can also explore for yourself some of the dynamics that we describe in greater detail (e.g. regional and seasonal trends in pricing and net load) in our interactive visualization tool of nodal electricity prices. To find more of our research on renewable energy visit us at Berkeley Lab's Electricity Market and Policy Department.

For questions, please contact Joachim Seel ([email protected]) or Dev Millstein ([email protected]) at Lawrence Berkeley National Laboratory.

We appreciate the funding support of the Solar Energy Technologies Office and the Wind Energy Technologies Office of the U.S. Department of Energy in making this work possible.