New Berkeley Lab study analyzes the financial performance of Connecticut solar leasing program that targets low- and moderate-income customers

Policymakers are increasingly interested in how to expand access to rooftop photovoltaic systems. In a study released today, Berkeley Lab analyzes the financial performance of a Connecticut Green Bank (CGB) solar leasing program, run in partnership with PosiGen, that targets low- and moderate-income customers. We show that this program has successfully reached underserved customers and has reasonable repayment rates given the credit characteristics of the participants.

The CGB/PosiGen program reaches many more underserved customers than other PV financing programs in Connecticut

The CGB/Posigen program is successfully reaching low- and moderate-income (LMI) households. The majority of CGB/PosiGen participants (58%) live in census tracts that have a median income of less than 80% of the area median income (AMI). In contrast, only 9% of participants in the other CGB solar financing programs live in these census tracts.

The majority of CGB/PosiGen participants (56%) have FICO scores that would generally be considered non-prime (<670), whereas only 2% of participants in the other programs have similarly low scores. All of CGB’s programs except PosiGen have minimum credit score requirements. Given their lower credit scores, many PosiGen participants would not qualify for other CGB products. The CGB/PosiGen program, therefore, has likely enabled access to rooftop solar for many of its participants.

Credit, not income, is the primary factor that explains participants’ financial performance

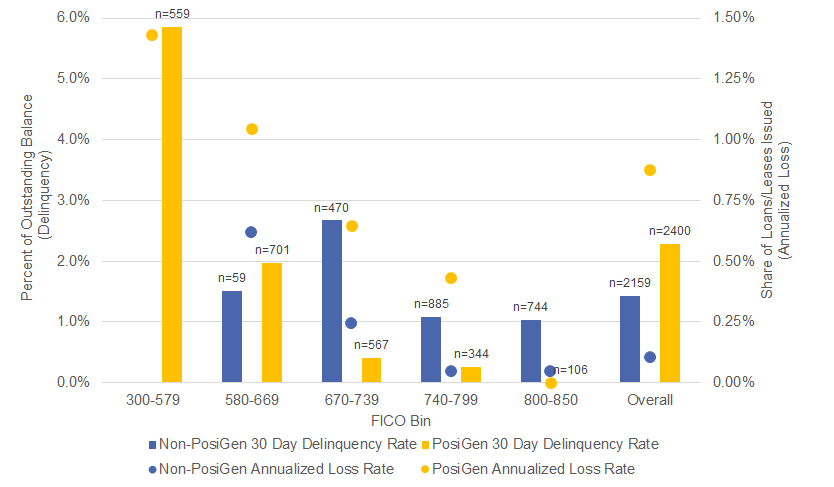

Overall, we find that delinquency and annualized losses are higher for PosiGen (2.3% and 0.9%) than for other CGB programs (1.4% and 0.1%). As the figure below shows, across the CGB programs, credit score has a strong relationship with lease and loan performance, with lower credit scores associated with higher rates of delinquency and loss. For example, a change in credit score of 117 points – the difference between the average credit score in the PosiGen program and the average score in the other CGB programs – would be expected to raise 30-day delinquency rates by 2.3% and the chance of being terminated early by 0.8%. CGB/PosiGen participants’ lower credit scores, therefore, explain much of the program’s higher rates of delinquency and annualized losses.

When we account for the impact of participant characteristics such as credit score, we find that PosiGen leases are 1.7% less likely to be 30 days or more delinquent and 2.6% more likely to be terminated early than the other CGB loans and leases. We also consider the impact of system size, principal amount, and census tract income on lease and loan performance but do not find statistically significant relationships.

PosiGen leases perform competitively with market-rate solar and non-solar leases and loans

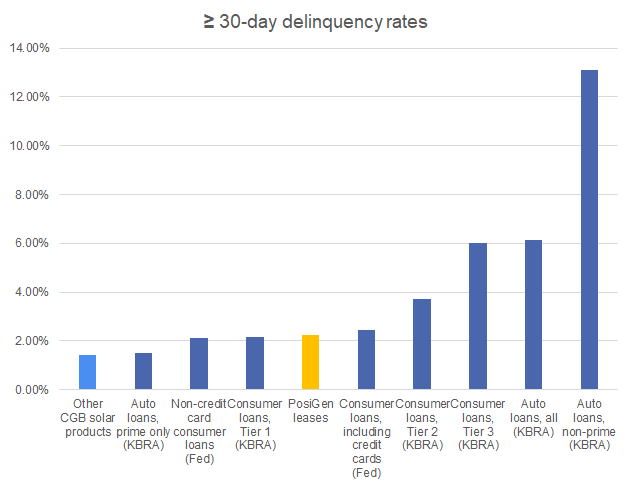

When compared to securities backed by market-rate PV loans and leases with similar amounts of seasoning, we find that the PosiGen leases have higher delinquency rates but comparable gross loss rates. The similarity in losses is notable given that loss rates for PosiGen leases were higher than those of the other CGB leases and loans. Rather than the PosiGen leases having high loss rates, other CGB leases and loans have unusually low loss rates. We also compare PosiGen to non-solar benchmarks, including indices of auto and consumer loans. We find that the PosiGen leases have significantly less delinquency than auto loans assessed by KBRA and have performance comparable to many consumer loans.