New Research Shows Energy Efficiency Loans Are Low Risk

Performance of energy efficiency loans is comparable to prime auto loans, ripe for growth and investment

A State and Local Energy Efficiency Action Network (SEE Action) study, recently announced by Department of Energy Secretary Granholm and developed by Lawrence Berkeley National Laboratory, shows that financial institutions can lend money to their customers for energy efficiency improvements at low risk in support of a more efficient building stock. While performance of energy efficiency lending has generally been understood to be strong, the data made available in this report significantly expands the volume and sophistication of the public evidence base through loan-level analysis of four large programs, three with track records of more than a decade and one that spans an economic cycle.

The study shows that some households from low-income areas take up energy efficiency loans, and that high-credit borrowers in these areas repay financing at a strong rate. Energy efficiency lending can help support policy goals related to equitable access to capital, such as the Biden Administration’s Justice 40 goals and Community Reinvestment Act compliance requirements.

The report reviews loan performance data for 52,511 energy efficiency loans from four long-running programs:

- The Connecticut Green Bank's Smart-E Loan program, which began issuing loans in 2013;

- The Keystone HELP program, run through the Pennsylvania Treasury, which began issuing loans in 2006;

- The Michigan Saves loan program, which began issuing loans in 2010; and

- The New York State Energy Research and Development Agency (NYSERDA)’s loan programs, which began issuing loans in 2010.

Loan performance

Across the four portfolios:

- Low Delinquency Rates: The 30-day delinquency rate – the share of outstanding loan dollars that are at least 30 days delinquent – is 1.57% (the 60-day delinquency rate is 0.62%, and the 90-day delinquency rate is 0.21%).

- Low Losses: Cumulative losses (charge offs) are highest early in loan lifetimes and decline later, a common finding for consumer loans. Our pooled portfolios lost 2.1% of the principal by year 2, 3.3% by year 4, 4.5% by year 6, and 5.1% by year 8.

- Credit Score Matters: Borrower credit scores are strongly associated with loan performance. Increasing borrower credit score by 100 lowers the odds that a loan is 30 days delinquent by 1.06 percentage points and the odds that a loan is charged off by 5.81 percentage points.

- Income is Less a Factor than Credit: Income metrics are also associated with loan performance. However, the association between income and loan performance is not nearly as strong as the association between credit score and loan performance. Credit score is a better predictor of loan performance than income.

Performance compared to other financial products

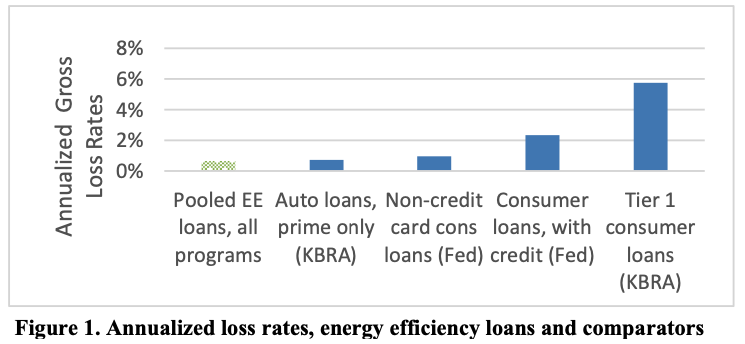

The studied energy efficiency loans’ performance compares favorably to other asset classes: their 0.65% annualized loss rate is comparable to prime auto loans (see Figure 1), which—unlike the efficiency loans—are secured. This strong comparative performance may be due to borrower characteristics or utility bill savings, or a combination of both. Regardless, these data provide the most comprehensive evidence to date that energy efficiency loans from programs such as these can be expected to perform well.

The studied energy efficiency loans’ performance compares favorably to other asset classes: their 0.65% annualized loss rate is comparable to prime auto loans (see Figure 1), which—unlike the efficiency loans—are secured. This strong comparative performance may be due to borrower characteristics or utility bill savings, or a combination of both. Regardless, these data provide the most comprehensive evidence to date that energy efficiency loans from programs such as these can be expected to perform well.

Find Long-Term Performance of Energy Efficiency Loan Portfolios online at: emp.lbl.gov/publications/long-

Find other SEE Action resources online at: https://www.energy.gov/eere/