Variable Renewable Energy Participation in U.S. Ancillary Services Markets: Economic Evaluation and Key Issues

As wind and solar energy become a larger share of electricity generation, there is growing interest in enabling these resources to provide reliability services to the grid through participation in ancillary services (AS) markets. Participation in AS markets could provide an additional source of revenue for resource owners to offset the declines in energy and capacity value that result from higher solar and wind penetration. It could also provide system operators with access to low-cost reliability services and a new tool for addressing emerging system constraints.

In the United States, participation by wind and solar generators in AS markets has been low to non-existent. Although there is no question that wind and solar resources are technically capable of providing reliability services, several questions around the economics of their participation in U.S. AS markets remain answered: What is the value to resource owners? Can wind and solar participation in AS markets provide high value to the electricity system as a whole, by offering services during periods of high AS prices? How do these values differ across different AS products, electricity markets, and between wind and solar generation, and how would they change with higher penetrations of wind and solar generation? What changes in electricity market rules would be needed to allow wind and solar generators to participate in AS markets?

This report examines the economic value of wind and solar participation in AS markets from resource owner and electricity system perspectives across the seven U.S. electricity markets. The analysis uses a price-taker dispatch model with historical market prices and simple, consistent assumptions that facilitate comparisons across technologies, wind and solar configurations, and markets over time. It considers two kinds of resources: standalone solar and wind generators, and solar and wind hybrid generators paired with battery storage.

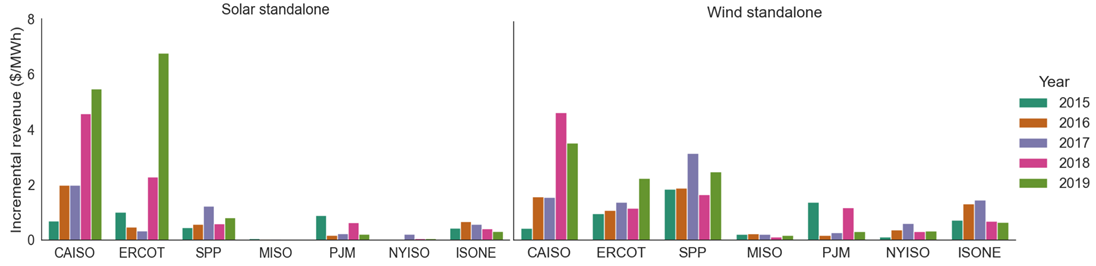

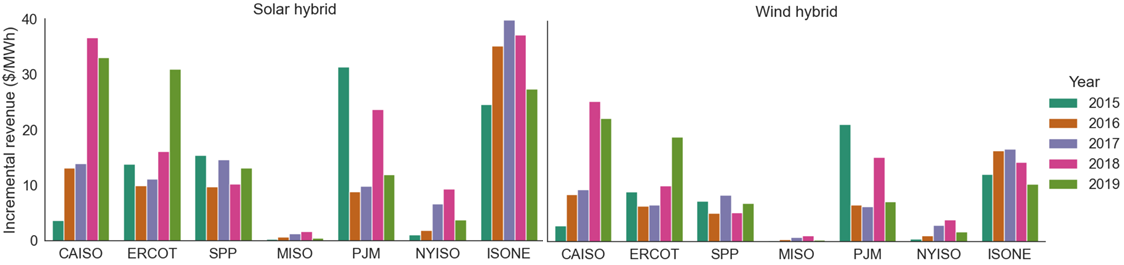

The analysis estimates additional revenues to standalone and hybrid solar and wind resource owners from participating in AS and energy markets, relative to only participating in energy markets. It focuses on markets for regulation reserves, which typically have the highest prices among AS products. Across electricity markets, we estimate that average (2015-2019) additional revenues from participating in regulation markets were $0.0-2.9/MWh (+0-15% of revenue without participation) for standalone resource owners and $1-33/MWh (+1-69%) for hybrid resource owners (see figures).

Figure: Incremental revenues to standalone solar and wind resource owners from AS market participation, 2015-2019 market prices

Figure: Incremental revenues to hybrid solar and wind resource owners from AS market participation, 2015-2019 market prices

The analysis also estimates the amount of regulation reserves provided by standalone and hybrid wind and solar facilities in each market and the average value of those reserves. In most markets, the value of regulation reserves provided by these resources exceeded average regulation market prices, indicating that they provided regulation reserves during periods with higher than average regulation prices.

Additional revenues and provision of regulation reserves were generally higher in markets with separate upward and downward regulation products (CAISO, ERCOT, SPP), relative to markets with a single bidirectional regulation product (MISO, PJM, NYISO, ISO-NE). Separate regulation products allow standalone and hybrid wind and solar facilities to provide regulation reserves more efficiently: because upward and downward regulation prices are weakly correlated, resources will most efficiently provide different levels of each product at different times.

Although the results suggest that, in some markets, there may be significant value to wind and solar resource owners from AS market participation, AS markets are relatively thin and have the potential to become saturated by energy storage projects that are currently in interconnection queues. Relying on additional AS revenues as a means to offset declining energy and capacity value may be a risky strategy for resource owners. The analysis considers sensitivities around provision of spinning reserves, point of interconnection limits, and higher penetrations of wind and solar generation.

The results offer two insights for independent system operators (ISOs) and regional transmission organizations (RTOs). First, they suggest that having separate upward and downward regulation products could enable more efficient provision of regulation reserves by wind and solar generators and energy storage. Second, they suggest that a first step toward enabling participation by wind and solar resources in AS markets may be to focus on hybrid resources, but that ultimately it may be beneficial to enable both standalone and hybrid wind and solar resources to participate in AS markets.

“Variable Renewable Energy Participation in U.S. Ancillary Services Markets: Economic Evaluation and Key Issues” was authored by Fredrich Kahrl of 3rd Rail Inc. and James Hyungkwan Kim, Andrew Mills, Ryan Wiser, Cristina Crespo Montañés, and Will Gorman of the Electricity Markets and Policy Department at Berkeley Lab.

We appreciate the funding support of the U.S. Department of Energy’s Office of Energy Efficiency and Renewable Energy.