Utility-Scale Solar Data Update

Utility-Scale Solar Data Update

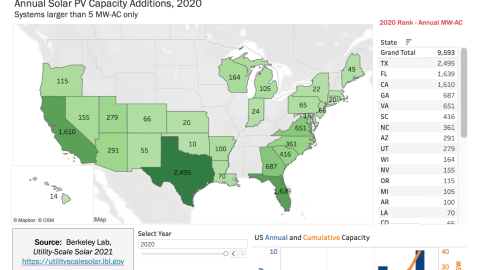

Lawrence Berkeley National Laboratory compiled and synthesized empirical data on the U.S. utility-scale solar sector. The focus is on ground-mounted systems larger than 5MAC, including photovoltaic (PV) standalone and PV+battery hybrid projects (smaller projects are covered in Berkeley Lab’s separate U.S. Distributed Solar and Storage annual data update). Data sources are diverse and include data from the Energy Information Administration (EIA), the Federal Energy Regulatory Commission (FERC), and state agencies. The latest update contains project-level data on 1,760 solar projects installed through 2024.

The update includes data synthesis covering:

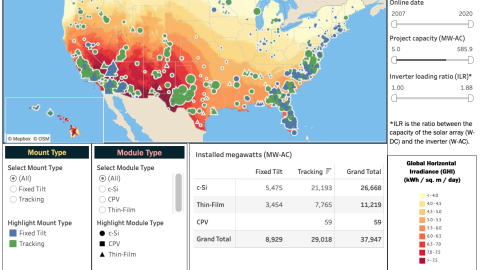

- Deployment and Technology Trends

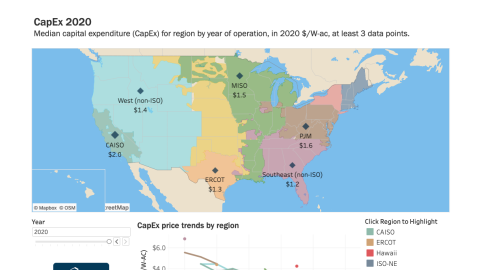

- Capital Costs (CapEx) and Operation & Maintenance (O&M) Costs

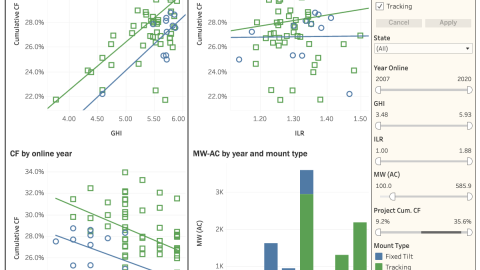

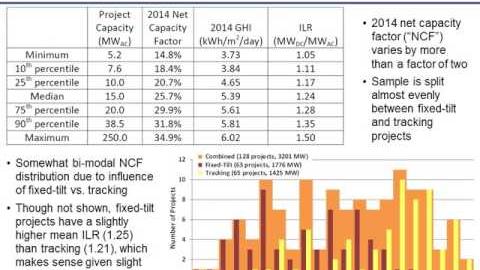

- Performance (Capacity Factors)

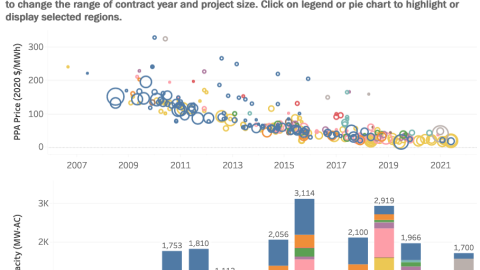

- Levelized Cost of Energy (LCOE) and Power Purchase Agreement (PPA) Prices

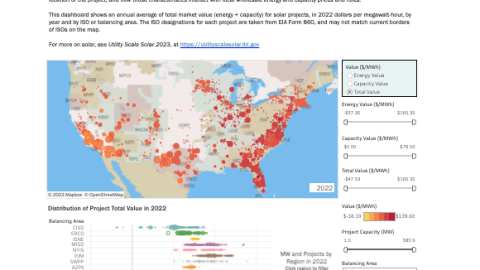

- Wholesale Market Value and Net Value

- PV+Battery Hybrid Plants (Deployment, CapEx, LCOE, PPAs)

- Concentrating Solar Thermal Power (CSP) Plants

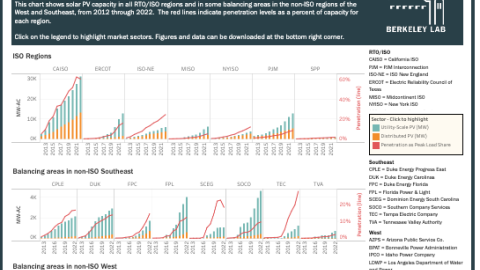

- Capacity in Interconnection Queues

These data are made available in several formats, including:

- A Public data file with non-confidential data on 57 tabs and additional visualizations,

- Data visualizations (click on Tools & Data in the tab above),

- Summary slide deck

In addition, plant-level hourly generation and annual value estimates are available for download at the Open Energy Data Initiative (OEDI) at https://data.openei.org/submissions/8541.

We want to hear from you. If you have specific questions about the data or requests for related analytical support from LBNL staff, you can contact Jo Seel and Julie Kemp.